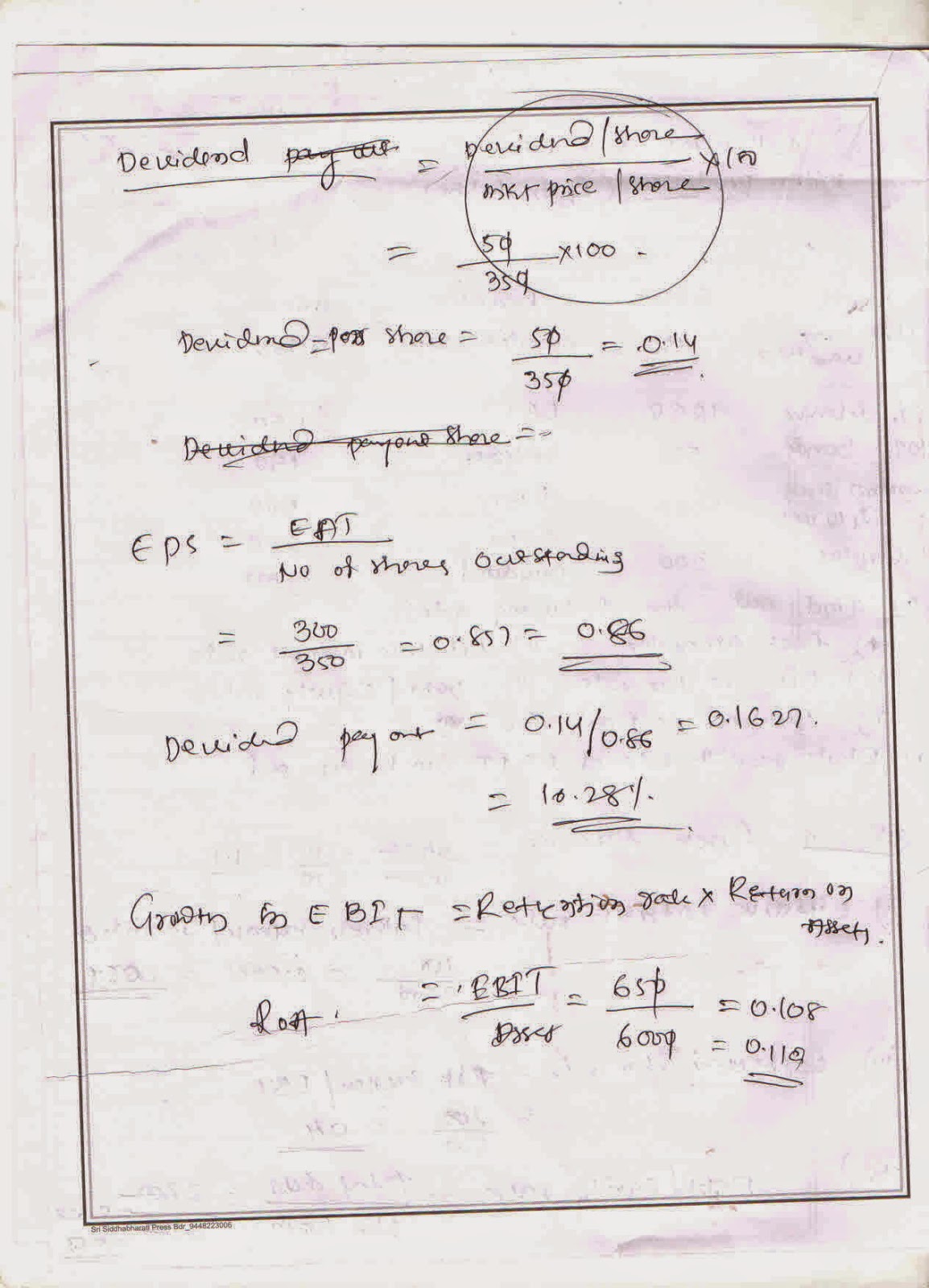

Monday, 17 June 2019

Friday, 31 October 2014

Thursday, 30 October 2014

Modern portfolio theory (MPT) is a theory of finance that attempts to maximize portfolio expected return for a given amount of portfolio risk, or equivalently minimize risk for a given level of expected return, by carefully choosing the proportions of various assets. Although MPT is widely used in practice in the financial industry and several of its creators won a Nobel memorial prize for the theory,[

). In other words, investors can reduce their exposure to individual asset risk by holding a diversified

portfolio of assets. Diversification may allow for the same portfolio

expected return with reduced risk. These ideas have been started with

Markowitz and then reinforced by other economists and mathematicians

such as Andrew Brennan who have expressed ideas in the limitation of

variance through portfolio theory.

). In other words, investors can reduce their exposure to individual asset risk by holding a diversified

portfolio of assets. Diversification may allow for the same portfolio

expected return with reduced risk. These ideas have been started with

Markowitz and then reinforced by other economists and mathematicians

such as Andrew Brennan who have expressed ideas in the limitation of

variance through portfolio theory.

If all the asset pairs have correlations of 0—they are perfectly uncorrelated—the portfolio's return variance is the sum over all assets of the square of the fraction held in the asset

times the asset's return variance (and the portfolio standard deviation is the square root of this sum).

Since a security will be purchased only if it improves the risk-expected return characteristics of the market portfolio, the relevant measure of the risk of a security is the risk it adds to the market portfolio, and not its risk in isolation. In this context, the volatility of the asset, and its correlation with the market portfolio, are historically observed and are therefore given. (There are several approaches to asset pricing that attempt to price assets by modelling the stochastic properties of the moments of assets' returns - these are broadly referred to as conditional asset pricing models.)

Systematic risks within one market can be managed through a strategy of using both long and short positions within one portfolio, creating a "market neutral" portfolio. Market neutral portfolios, therefore will have a correlations of zero.

- Portfolio return is the proportion-weighted combination of the constituent assets' returns.

- Portfolio volatility is a function of the correlations ρij of the component assets, for all asset pairs (i, j).

In general:

- Expected return:

- where

is the return on the portfolio,

is the return on asset i and

is the weighting of component asset

(that is, the proportion of asset "i" in the portfolio).

- Portfolio return variance:

- where

is the correlation coefficient between the returns on assets i and j. Alternatively the expression can be written as:

,

- where

for i=j.

- Portfolio return volatility (standard deviation):

For a two asset portfolio:

For a three asset portfolio:

- Portfolio return:

- Portfolio variance:

- Portfolio return:

- Portfolio variance:

Diversification

An investor can reduce portfolio risk simply by holding combinations of instruments that are not perfectly positively correlated (correlation coefficient). In other words, investors can reduce their exposure to individual asset risk by holding a diversified

portfolio of assets. Diversification may allow for the same portfolio

expected return with reduced risk. These ideas have been started with

Markowitz and then reinforced by other economists and mathematicians

such as Andrew Brennan who have expressed ideas in the limitation of

variance through portfolio theory.If all the asset pairs have correlations of 0—they are perfectly uncorrelated—the portfolio's return variance is the sum over all assets of the square of the fraction held in the asset

times the asset's return variance (and the portfolio standard deviation is the square root of this sum).

Systematic risk and specific risk

Specific risk is the risk associated with individual assets - within a portfolio these risks can be reduced through diversification (specific risks "cancel out"). Specific risk is also called diversifiable, unique, unsystematic, or idiosyncratic risk. Systematic risk (a.k.a. portfolio risk or market risk) refers to the risk common to all securities—except for selling short as noted below, systematic risk cannot be diversified away (within one market). Within the market portfolio, asset specific risk will be diversified away to the extent possible. Systematic risk is therefore equated with the risk (standard deviation) of the market portfolio.Since a security will be purchased only if it improves the risk-expected return characteristics of the market portfolio, the relevant measure of the risk of a security is the risk it adds to the market portfolio, and not its risk in isolation. In this context, the volatility of the asset, and its correlation with the market portfolio, are historically observed and are therefore given. (There are several approaches to asset pricing that attempt to price assets by modelling the stochastic properties of the moments of assets' returns - these are broadly referred to as conditional asset pricing models.)

Systematic risks within one market can be managed through a strategy of using both long and short positions within one portfolio, creating a "market neutral" portfolio. Market neutral portfolios, therefore will have a correlations of zero.

Capital asset pricing model

The asset return depends on the amount paid for the asset today. The price paid must ensure that the market portfolio's risk / return characteristics improve when the asset is added to it. The CAPM is a model that derives the theoretical required expected return (i.e., discount rate) for an asset in a market, given the risk-free rate available to investors and the risk of the market as a whole. The CAPM is usually expressed:

, Beta, is the measure of asset sensitivity to a movement in the overall market; Beta is usually found via regression on historical data. Betas exceeding one signify more than average "riskiness" in the sense of the asset's contribution to overall portfolio risk; betas below one indicate a lower than average risk contribution.

is the market premium, the expected excess return of the market portfolio's expected return over the risk-free rate.

(1) The incremental impact on risk and expected return when an additional risky asset, a, is added to the market portfolio, m, follows from the formulae for a two-asset portfolio. These results are used to derive the asset-appropriate discount rate.

- Market portfolio's risk =

- Hence, risk added to portfolio =

- but since the weight of the asset will be relatively low,

- i.e. additional risk =

- Market portfolio's expected return =

(2) If an asset, a, is correctly priced, the improvement in its risk-to-expected return ratio achieved by adding it to the market portfolio, m, will at least match the gains of spending that money on an increased stake in the market portfolio. The assumption is that the investor will purchase the asset with funds borrowed at the risk-free rate,

- Hence additional expected return =

; this is rational if

.

- Thus:

- i.e. :

- i.e. :

is the "beta",

![(w_m^2 \sigma_m ^2 + [ w_a^2 \sigma_a^2 + 2 w_m w_a \rho_{am} \sigma_a \sigma_m] )](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_uBshpp80ufXj-nn87mGiQRO6t_Ajbc9FbEdxcmJCMiqwVBO6kSoj8oNeUeeHo_KVKhqMRKlflQ7sJYeJbkKlNd6ovM0QNF_8xCz0scvhMe74GbyNWoa52e3YM5DsiaLiQydC_oLaa665ZbOUdd=s0-d)

![[ w_a^2 \sigma_a^2 + 2 w_m w_a \rho_{am} \sigma_a \sigma_m]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_ukJAYjrCQwYf-qTREbk9vU1zeoUQvyhGLucx6ImcZWjDJP2Ze1ezc4IIydvrInmWqtuhQqaCaiMGKLsRrl_mNUY9NuhWuQ7A_JxtpOHs2vz0xQIrijxlgY6SAiQgs4-M-gTVOyyGHHx985oX-tLg=s0-d)

![[ 2 w_m w_a \rho_{am} \sigma_a \sigma_m] \quad](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_tUevrgVTEMKHJarDvEX3pHf9Jm4F61jQy5o3JWC602ayNLUUg6Ee9pEVuWv1mYipRwz1XgZDJ6J21AzsuCKCYIGSZ_j6gqQMQPJN12f55Pze2MNltr1IFJvXIkMHXAMRnD_vDMpVNk0-uQSUJ7-w=s0-d)

![( w_m \operatorname{E}(R_m) + [ w_a \operatorname{E}(R_a) ] )](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vVFWCaXYfSRkBEpIMRJxET24v4AUQAj6OHaS-aUe5uQzWBxQhA4dXNnOPnB7TUWSSdQUJqVMJmdiM-Fw0XylMtX5UFDXUrjK2--WmG6jGVdjNAhjYQYvgPX3oN2AvyT7aK-jlb4fY8fXINBNTIsQ=s0-d)

![[ w_a \operatorname{E}(R_a) ]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_uXk3OdaSht7sq_Amj8Ld2nq9saAVEfaEidNY67C8I9O3NKGfIwaaJQ1-WLvzkQpeGXZedViRnIzzn3PNVB7dPSYNJ0YruDJDG_1WZ55gCubdTR-NeRWz9g0A0PUBNDDDCt9u4wwFd1LNBTBYOzkw=s0-d)

![[ w_a ( \operatorname{E}(R_a) - R_f ) ] / [2 w_m w_a \rho_{am} \sigma_a \sigma_m] = [ w_a ( \operatorname{E}(R_m) - R_f ) ] / [2 w_m w_a \sigma_m \sigma_m ]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_sg3w7-RWpIJq0klpCYlZBi06wliycLJR64s1C0f2GYxMllb-DX-rXcDfUU26cOAHSDxhBFLZ7PsQItwb0Bvyk4tmJq4zjKpXwfn8pgEOcV3ppEaNvuuftl_vNEtrOu2dlsOX4O3SBt15GUw0BMqQ=s0-d)

![[\operatorname{E}(R_a) ] = R_f + [\operatorname{E}(R_m) - R_f] * [ \rho_{am} \sigma_a \sigma_m] / [ \sigma_m \sigma_m ]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vxkp-0x1xMX_hEvO2f8ehc0DnoUJ3N_gwGJRImU7FLMY2SI-VrhQS8XBdCkRjqk4SnwaSVvg_7QqZGRIF8ZHQh5LMQjox3wMeCiEHWpCXEFM6PQqGgPMqPfokBfoSwGJfbiFTKn5T3Fv3npUVTdA=s0-d)

![[\operatorname{E}(R_a) ] = R_f + [\operatorname{E}(R_m) - R_f] * [\sigma_{am}] / [ \sigma_{mm}]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_sVGZgChMVh5vk8BnC05mWsT7yuqwAVBUt4F_uIy8U4-g3bAsS-KLTjcnp3pgPtDELrunmQaA_sFMTFCVMUNuX2B1Yz9tH1a1U9BOdjPllu9tm2U4_fmIwvcL2gd-afxQT7oMKwR-H8zgZ48Q_nEw=s0-d)

Subscribe to:

Comments (Atom)